In the second half of 2019, the Commonwealth Government commissioned the Retirement Income Review to “establish a fact base of the current retirement income system that will improve understanding of its operation and the outcomes it is delivering for Australians”.

This review was handed to the Government back in July, but thus far they have resisted calls to make the report public. Unfortunately, such a ‘fact base’ is sorely needed right now. The 2020-21 Budget contained a number of reforms to superannuation with far-reaching consequences. As the public digests these changes and legislators contemplate their decisions, the absence of an independent fact base continues to hamper their ability to scrutinise claims being by made by the different sides of the debate.

While Australians wait for the review to be released, it’s still important to take a look at some of the myths perpetuating in the debate about superannuation. In this first instalment, we examine fees in the superannuation system, specifically we seek to understand who might be paying too much and whether the proposed reforms in the Budget can be expected to have a significant impact on the $30 billion Australians pay in fees every year.

For good reason, much of the debate about superannuation focuses on fees. The nature of compound interest can result in small increases in fees, turning into significant reductions in ultimate retire savings. The Productivity Commission estimated that paying 0.5% in higher fees over your working life will decrease your final super balance by the equivalent of 2 years’ of pay.

It is becoming increasingly common to hear policymakers and commentators talk about how much we are paying for fees each year. So much so– even the Government’s factsheet on the superannuation reforms in the 2020-21 Budget is centred around the $30 billion in superannuation fees Australians are paying each.

However, this headline figure still leaves questions to answer. Particularly, the question is left open as to whether this is a universally shared experience, or an unlucky minority is getting gouged. Additionally, will the Government’s reforms do much to bring fees down?

Retail funds & low balance SMSFs have the highest fees

To understand the various fees Australians are paying, and whether they’re getting value for money, it makes sense to start by looking at the different segments in the system. Under Australia’s defined contributions system, superannuation is held in either a MySuper account (the most tightly regulated), a Choice account or a Self-Managed Superannuation Fund (SMSF):

- MySuper segment – products with a single, diversified investment strategy and few other features except insurance. Trustees have fiduciary duty to act single mindedly in the best financial interests of members. Default contributions must be to an eligible MySuper fund.

- Choice segment – investment choices are not restricted and therefore members would bear substantial responsibility and the emphasis of trustee responsibilities placed on disclosure rather than a fiduciary duty.

- SMSF segment – members are self-reliant in making investment decisions and while they can access professional support and advice they are responsible for outcomes.

Comparing fees or costs on products in different segments can be problematic. For instance, the Productivity Commission points out that expenses reported to the Australian Taxation Office (ATO) for SMSFs won’t include each member’s own time spent managing their investments. Notwithstanding these gaps, the Productivity Commission does provide estimates of the average fees or costs in each segment and we have used these to get a sense of how much each segment contributes to the $30 billion total.[1]

[1] The Productivity Commission’s report used had 2017 data for the Choice and MySuper segments but only 2016 data for SMSFs, based on ATO data available this is expected to underestimate the SMSF share. Public Sector defined benefit products have been excluded.

It shows quite starkly that the MySuper segment had the lowest fees and that as a result they contribute to just 20% of the total fees in the system. In contrast, SMSFs contributed 31% of the fees paid by members and Choice products contributed to 49%.

If we want to drill down into each of these sectors, we find the picture is not uniform.

For instance, the Productivity Commission showed that SMSFs which typically face higher fixed costs can be quite efficient when the balance of funds is high. On the other hand, when the balance is lower than $500,000 the data tells a different story.

Using Australian Taxation Office (ATO) data for 2017-18 we have been able to estimate the minimum fees for operating an SMSF and see how they vary depending on the size of the fund.

This shows that for the 74 per cent of SMSFs with balances of less $500,000, the costs of managing the fund are likely to be significantly higher than the costs of most Choice and MySuper products. Meanwhile the nearly 39 per cent of funds with less than $200,000 are paying effective fees of at least 5.1 per cent.

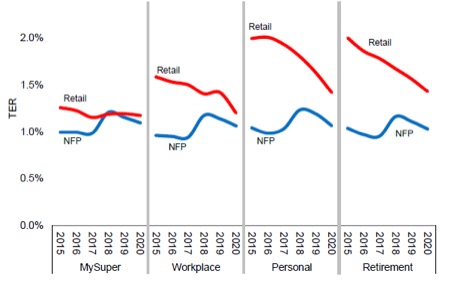

A lack of uniformity can also be found amongst APRA-regulated funds. Rainmaker Information has produced detailed analysis that compares funds in the retail sector with those in the not-for-profit or profit-to-member sector[1]. It shows that over the last five years:

- Within the MySuper segment, fees charged in both sectors have largely converged.

- Across MySuper and Choice products, fees charged by the profit-to-member sector are largely consistent.

- For the retail sector, fees vary considerably across all segments. And whilst they have come down, they remain higher in Choice segments particularly those accounts where the member has joined the fund from outside the industrial relations system.

This is consistent with the observations by the Productivity Commission that most high-fee products are retail products in the choice segment, representing 17 per cent of assets under management in 2017. In examining the underlying structure of fees that the main driver of higher fees for these significantly higher administration fees.

When you look into the variation in fees across the system, it’s easier to see that some people are paying more reasonable fees than others. Policymakers should take this into account in any efforts to help those with high fees. Particularly, any serious policy should include measures targeted at the following two areas:

- The creation of high-cost SMSF accounts with balances lower than $200,000.

- The high levels of fees charged in the Choice segment, informed by an understanding of why fees charged by Retail funds are systematically higher.

Budget 2020 won’t do anything to address the highest fees

The Government’s information paper estimates that the total benefit to Australians from the four measures contained in the Budget will be $17.9 billion over the next ten years. While detailed modelling is not provided, a measure worth $10.7 billion is related to improved investment performance. This leaves at most $7.2 billion of benefits that might come in the form of lower fees.

On an annualised basis and assuming even growth over time,[1] this suggests at most these reforms will deliver a 2% reduction in total fees, or the equivalent of reducing them from $30 billion to $29.4 billion. However, since these measures also include benefits caused by improved investment performance, the reduction in fees will be lower than this.

In terms of targeting, if we look at how three measures treat the three segments of the sector we can see that only one of the measures incorporates either of the segments with the highest fees:

If we look further at the proposed formula for benchmarking of fund performance and fees we see that they only include investment fees for each asset class and exclude administration fees despite these being the major contributor of excessive fees in APRA-regulated funds.

So with SMSFs excluded entirely and Choice products only included for the increasing transparency and accountability measures and administration fees excluded from the benchmarking, the measures appear to be poorly targeted. This might explain why the Government is only aiming to achieve modest reductions of less than 2 per cent over the next decade.

To put this into context, if a reform package was developed with the aim of brining Choice fees and SMSF costs into line with MySuper accounts that would reduce fees by 19 per cent or equivalent of bringing the total bill down to $24.3 billion. Over 10 years, that would deliver savings of up to $67 billion.

Proponents for these changes may argue that people in Choice products or SMSFs made an informed choice to be there and therefore we don’t need worry about protecting them. If that is the case then the fees on those should also be excluded from the policy discussion to justify these reforms, and we should instead should just be focusing on the $5.4 billion in fees charged on MySuper accounts.

In reality, we should be looking at the cost of the entire system, which ultimately also means examining how ‘informed’ individual choices really are in practice. But that’s a super myth for another time.

SOCIAL SHARE